Beware of credit offers via Facebook, LinkedIn, WhatsApp & Co.

On the internet and in social media, criminals repeatedly try to exploit people's financial distress in order to make a quick buck.

The scam works with specially set up websites, advertisements or comments promising cheap, easy or SCHUFA-free loans from banks and intermediaries from other EU countries or from private individuals.

Fake profiles and false promises

The scam is particularly common in social networks such as Facebook, LinkedIn, Instagram or Pinterest. However, the European Consumer Centre (ECC) Germany has also received cases in which people were contacted proactively via WhatsApp or calling up websites of supposed banks or credit brokers themselves.

The usual approach: Criminals create fake profiles or pages with a false identity on Facebook, for example. Then they send out friend requests en masse.

Those who accept them will receive private messages from people who have allegedly successfully obtained a loan from s specific credit broker.

Another example: Comments are posted with loan offers from supposed banks from other EU member states.

They always lure their victims with large sums of money, low interest rates and loose conditions for granting credit. It is often advertised that the loan is “SCHUFA-free”.

The wording could be as follows:

Are you looking for a loan? We offer you a loan between 5,000 and 100,000 euros. And that with only 2 % interest. So, you will be able to pay your debts and don't have to worry. Interested? Then contact us: Email (...) or WhatsApp + (...)

What is the SCHUFA?

SCHUFA is a German company with the task of providing its contractual partners with information on the creditworthiness of customers and thus protecting them from losses.

For this purpose, data from credit contracts and payment behaviour are collected and evaluated.

A SCHUFA-free loan would thus be a loan that does not count towards the SCHUFA score and thus does not influence your personal credit rating.

Click here to go to the SCHUFA website.

Fraud features: Strange credit contracts and prepayment

People who are already in a financial emergency and cannot get a loan from their bank feel attracted by such offers and sense a chance to easily get a loan.

Those who make contact are lured into the trap with "nice words" and skilful conversation, as consumers report to the ECC.

A lively correspondence follows. Credit offers are made and even a contract is sent. At this point at the latest, caution is advised.

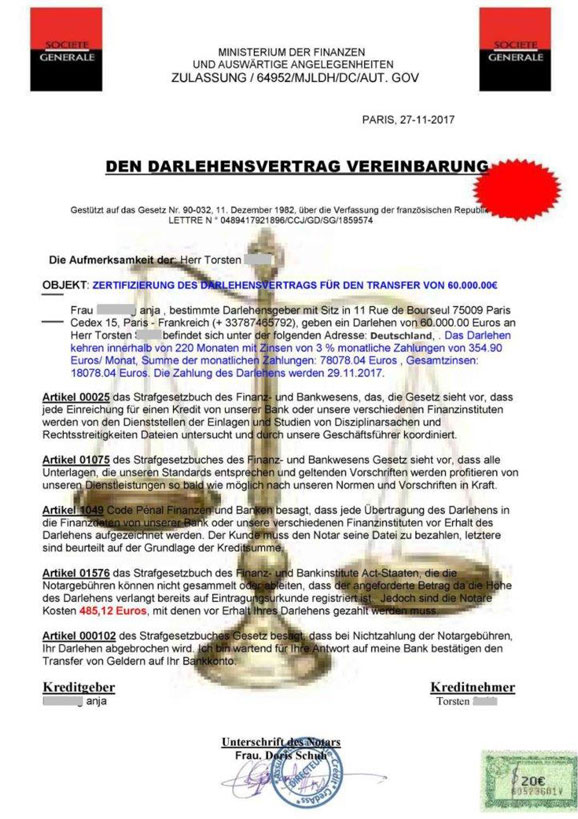

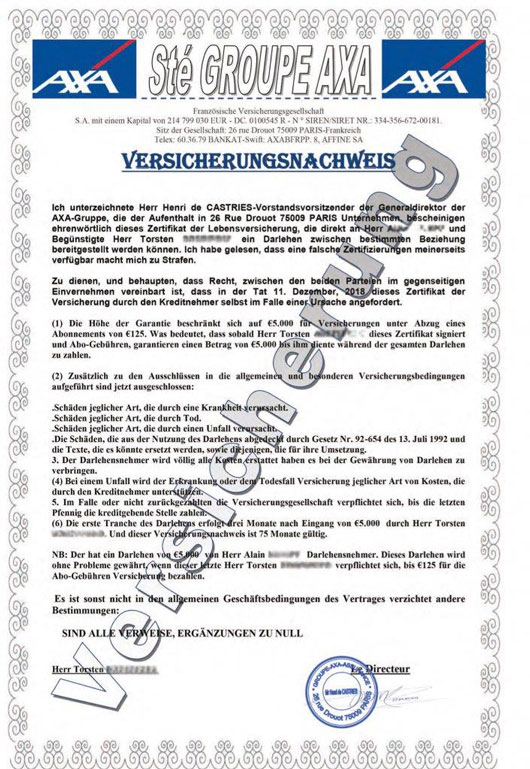

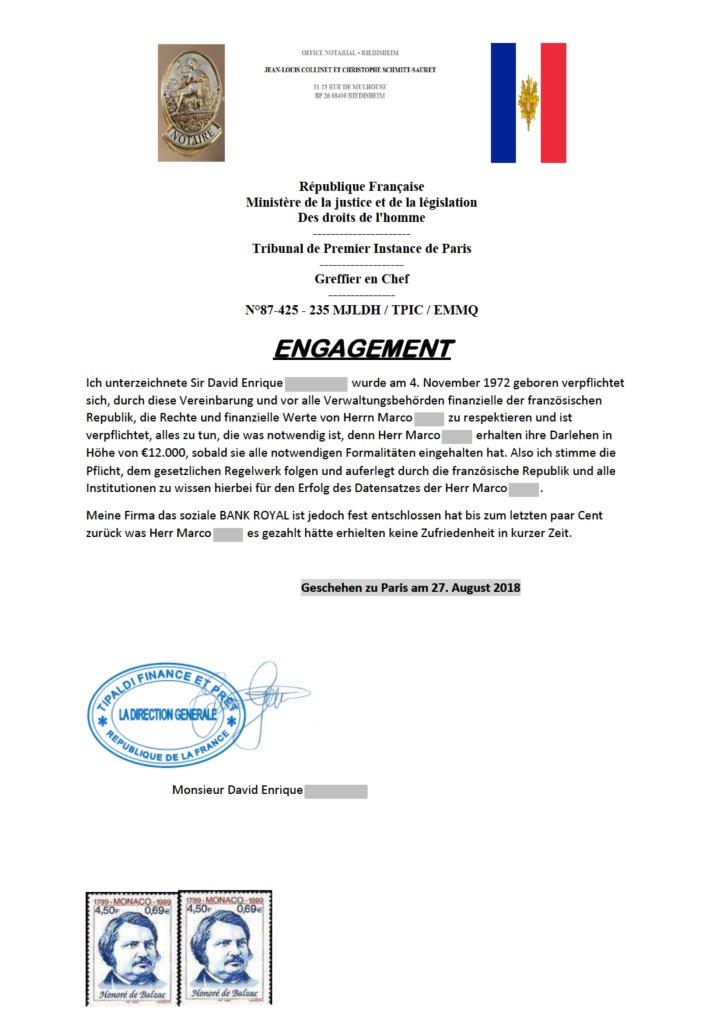

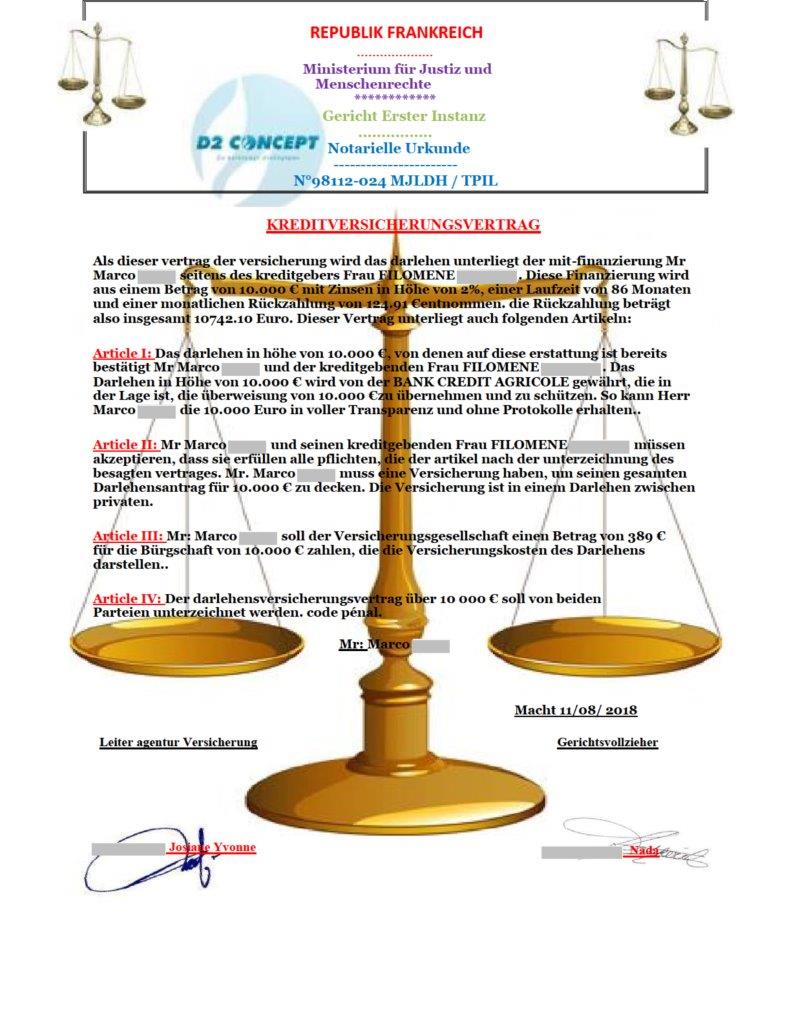

The contracts often appear unprofessional and amateurish. Indications of this are, for example, questionable designs and poor German.

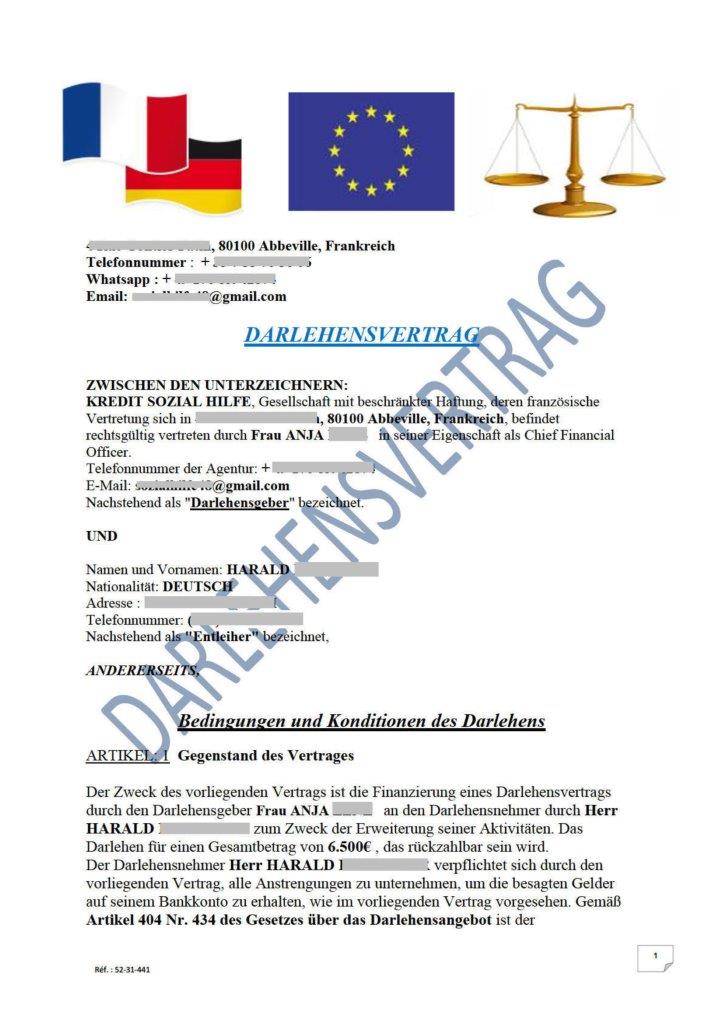

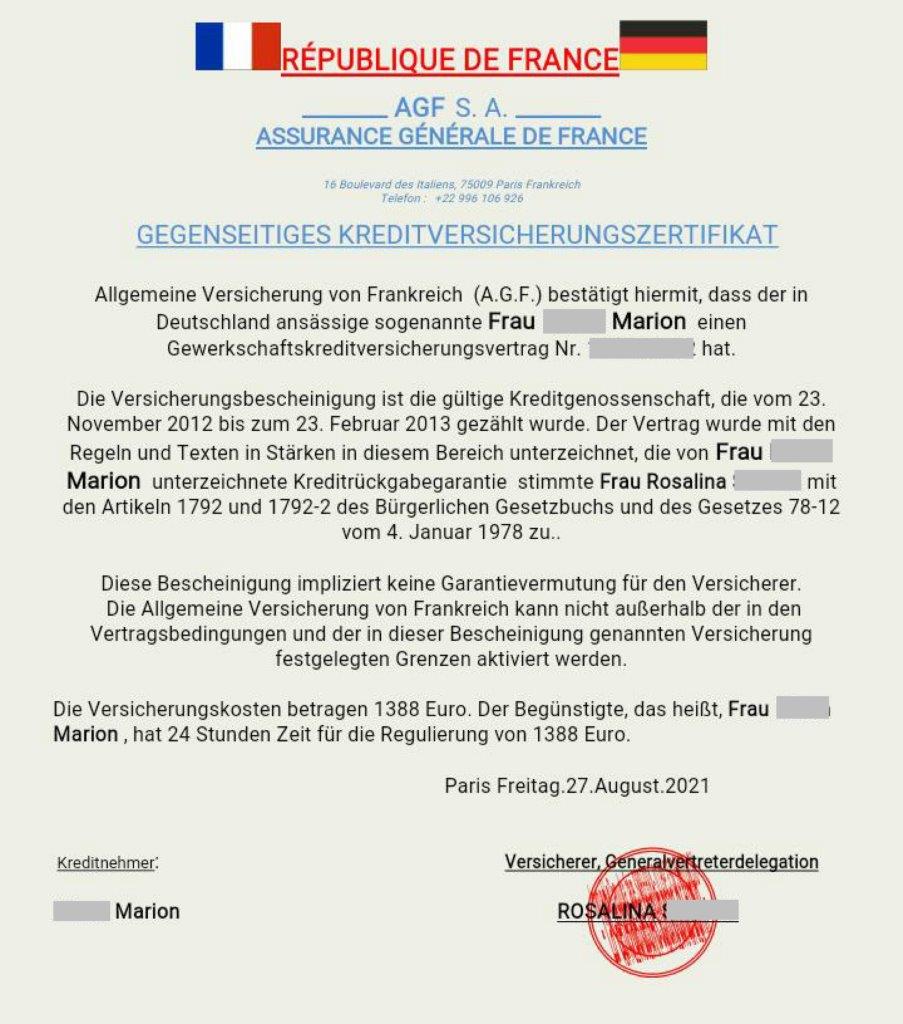

In some cases, logos of foreign ministries, well-known banks or insurance companies are also copied in and misused (see examples of fictitious credit agreements below).

Alarm bells should ring at the latest when the transfer of a certain amount of money is requested before the loan amount is disbursed, for example for alleged processing fees, taxes, money laundering certificates, clearance by authorities or notary fees.

Those who pay are usually confronted with further payment demands.

This goes on until the fraudsters notice that their victim becomes sceptical or simply has no more money left. If the victims stop the payments or ask too many questions, they usually just hear nothing more from the criminals. They have fallen for a so-called advance payment scam (in German: “Vorschussbetrug”).

Important: No matter how much you pay, you will never receive the allegedly approved amount. So, keep your hands off supposedly credit history-free or particularly favourable loans!

How to protect yourself from credit fraud

- Ignore credit offers on Facebook, WhatsApp, Instagram, LinkedIn etc. It is a scam. Reputable banks would never make concrete offers via social media.

- Banks or credit agencies do not use email addresses that can be created by anyone, such as gmail, gmx, etc.Do not tell strangers about your financial situation.

- Do not enter into contracts with people you do not know.

- Do not disclose personal information on social media channels.

- Never pay via cash transfer services such as Western Union, MoneyGram or with vouchers/payment cards such as "Paysafe" or by real-time bank transfer.

- Check the "Impressum" of the website to see where the lender is based and check with the national supervisory authority whether the company actually exists and is authorised to broker loans. BaFin, the Federal Financial Supervisory Authority in Germany, provides an overview of all European supervisory authorities. On the page of the respective supervisory authority, you can find out whether the provider is authorised. Do not find any information: Hands off! If in doubt, you can also ask the European Consumer Centre Germany for advice.

What is an Impressum?

An “Impressum” is a legally mandated statement of the ownership and authorship of a website, which must be published or otherwise made available to consumers in Germany.

It is often found at the bottom of the website.

How to recognise credit fraud

- Contact via WhatsApp, social media or email.

- Unusual promises are made (low interest rate, no credit check, credit from private individuals).

- Victims are always asked to pay different fees, before they supposedly receive the loan (which never happens): taxes, administration fees, activation codes, money laundering certificates, insurance, ...

- A supposed lawyer or notary is interposed for the settlement.

- Often bumpy and incorrect German in advertisements and fake profiles.

- Use of a private email address or telephone number for communication.

- New Facebook friends report alleged success stories about a loan.

- Victims will be sent a copy of the alleged clerk's identity card to establish the seriousness of the transaction.

- Victims receive access data to a supposedly personal user account on a website where you can see the supposed approval procedure for the loan. Attention: this says nothing about the seriousness! Nowadays, anyone can put such a website online within a few hours. No "official" body checks whether it is actually a bank or similar.

You will quickly realise that you have already made contact with crooks, because scammers

- usually answer promptly, but possibly at unusual times that do not correspond to the opening hours of a bank,

- quickly demand personal data such as bank details and copy of ID or payslip,

- send out strange and colourful contracts,

- would like to install a remote maintenance programme (such as "TeamViewer") on your computer and "help" you transfer the sums,

- build up time pressure,

- charge a fee before disbursement, e.g. processing fees or credit information fees,

- require you to open a bank account via “Videoident” procedure and transmit the access data to the alleged lenders.

Fooled by a scam. What now?

- Immediately report the incident to the police. This can be done at any police station nearby.

- Block email senders and phone numbers on your terminals if you suspect a scam.

- If your account has been hacked, you should also report this to the social platform. Change your password if still possible. Use strong passwords consisting of numbers, letters, special characters and upper and lower case letters.

- If you have sent the perpetrators a copy of your identity card or passport, you should withdraw this document from circulation as soon as possible by having a new one issued. In addition, we recommend filing a charge of identity theft in addition to the charge of (attempted) fraud. German consumers can also report identity theft to SCHUFA as a precaution.

- Watch your account activity in the near future in case you have disclosed your bank or credit card details.

- You should also react immediately if you receive invoices but no goods or if you have not ordered the goods at all. The perpetrators may go on a shopping spree in your name.

- Victims are often threatened when the perpetrators realise that they will not pay any more money. Do not be impressed by this. You have not entered into any legally binding commitment and are not obliged to pay.

- If you open an account via Videoident but no longer have access to it, you should inform the bank immediately.

- If in doubt, you can also ask the European Consumer Centre Germany for advice.

Examples of invented credit agreements

Funded by the European Union. Views and opinions expressed are however those of the author(s) only and do not necessarily reflect those of the European Union or the European Innovation Council and Small and Medium-sized Enterprises Executive Agency (EISMEA). Neither the European Union nor the granting authority can be held responsible for them.